The Consumer Costs and Climate Impacts of the Renewable Fuel Standard

Author

Read the Series

Introduction: The Cost of Renewable Fuel Incentives: A Two-Part Policy Analysis Series

Part II: How the RFS Has Damaged the Environment and Burdened Taxpayers

Media Contact

For general and media inquiries and to book our experts, please contact: pr@rstreet.org.

The RFS should be repealed so that the market—rather than politicians—can determine the optimal level of ethanol-gasoline blending.

Introduction

In 2005, to address energy security and climate concerns, the United States adopted a program intended to supplant the need for imported oil with domestic renewable fuels. This program—the Renewable Fuel Standard (RFS)—was expanded in 2007 to create both an explicit greenhouse gas (GHG) abatement component and to statutorily mandate that increasingly large volumes of renewable fuel be blended into the domestic fuel supply. Most of this renewable fuel has come in the form of conventional ethanol produced from corn.

Because of the RFS, the United States grows considerable volumes of corn expressly for fuel production. It is estimated that approximately 40 percent of all corn grown in the United States is used for ethanol. But whether this program incurs a cost or provides a benefit to Americans has been a hotly debated topic. Some argue that the program has little cost, as there is considerable demand for ethanol as a liquid fuel regardless of whether the RFS exists or not. To this point, a certain amount of ethanol blending is to be expected regardless of policy directives, as ethanol has a higher octane than gasoline, which can help improve engine performance. But ethanol itself has a lower energy density than gasoline, meaning that fuel mixtures with higher levels of ethanol reduce fuel efficiency.

On the other hand, parts of the world that do not have mandates for ethanol consumption but that also have high gasoline prices, like Europe, do not blend ethanol into their fuel supplies at the same rate as the United States. This indicates that the RFS is forcing a greater consumption of ethanol than the market would pursue normally. As such, the RFS likely results in increased costs to consumers, particularly from increased food and fuel costs.

This analysis aims to estimate a portion of costs consumers have paid for the RFS based on the higher energy cost of ethanol relative to gasoline, as well as a portion of the compliance cost of the program that can be gleaned from the market where credits demonstrating compliance are traded. Additionally, in estimating these costs, it becomes possible to assess the overall abatement cost of the conventional fuel portion of the RFS to help determine whether it is a cost-effective climate program.

Overall, our research suggests that the volume of ethanol consumption required by the RFS was likely considerably above what would have otherwise been consumed. Furthermore, we find that in most years of the RFS’s existence, ethanol cost more per unit of energy than gasoline and involved considerable program compliance costs that were passed on to consumers. This combination of factors, therefore, leads us to conclude that the RFS has resulted in significant costs to consumers in the form of higher fuel expenditures.

Cost to Consumers

To assess the RFS’s overall cost to consumers, we must first estimate the amount of ethanol that would have been consumed if the program had not been implemented. Unfortunately, there is a dearth of data to draw from in this regard. Although the U.S. government has attempted to estimate the economic impact of the RFS, these estimates have suggested very low program implementation costs because the calculations have assumed that large quantities of ethanol would have been consumed regardless of whether or not the RFS was implemented. If this assumption were true, the RFS would, in fact, have incurred little cost to consumers.

However, an alternative assumption to consider is that ethanol consumption as a share of finished motor gasoline (i.e., gasoline that is blended with ethanol) would have remained closer to pre-RFS levels (around 3.5 percent, compared to the present-day 10 percent). This view is supported by the fact that Europe—a region that faces much higher gasoline prices than the United States—typically only blends ethanol to a volume of 5 percent of finished gasoline.

Methodology

For our analysis, we assumed that—had the RFS never been implemented—the consumption of ethanol would have been primarily determined by the desire for higher octane ratings and to avoid consuming potentially higher-cost gasoline. That is, if gasoline costs were to rise, the market would seek to replace more of it with ethanol, but if gasoline costs were to fall, then less ethanol would be consumed. As such, we assumed that a blend rate of 5 percent ethanol in finished gasoline would have been the norm had the RFS not been adopted, consistent with the blend rate observed in Europe where gasoline prices are higher than they are in the United States.

To estimate the direct costs incurred by consumers from the RFS, we looked at two factors: (1) the higher cost that consumers have paid for the mandated consumption of ethanol instead of gasoline and (2) the price paid for the RFS’s compliance mechanism of Renewable Identification Numbers (RINs) (the credits refiners use to show compliance with the RFS, which are traded in markets). Estimating these values enables us to approximate the cost that consumers have paid for the RFS.

We assumed that from 2010 to 2023, a 5 percent blend rate of ethanol in finished motor gasoline would have been the norm, and the difference in this 5 percent blend rate and the RFS blending requirement represents additional ethanol consumption induced by the program. We then estimated what it would have required to meet the same energy demand via conventional gasoline, which is more energy dense. Using historical data for wholesale ethanol prices and conventional gasoline prices from the U.S. Energy Information Administration (EIA), we then calculated the consumer cost paid for energy under the RFS as the difference between the cost of supplying energy as gasoline compared to the cost of supplying energy as ethanol.

Additionally, we estimated the cost of complying with the RFS program by comparing RIN prices to blend obligations. Specifically, when ethanol is produced, a RIN is also produced, and fuel refiners purchase RINs to demonstrate compliance with the RFS program. The cost of purchasing these RINs is passed along to consumers as a form of tax and to ethanol producers as a subsidy. Importantly, even in cases where refiners are able to blend ethanol into gasoline without purchasing RINs on the open market, there is still a cost that is passed through to consumers from the implicit value of the RIN, as noted by the EPA. For conventional ethanol, a D6 RIN is used for program compliance, and we used EPA data on RIN prices as well as RFS blending requirements to derive an estimate of the total expenditure for conventional biofuel RINs. We assumed that this cost was passed on to consumers at the pump, which represents an additional compliance cost of the program.

We calculated the total cost to consumers from the program as the additional cost paid for a less efficient form of energy, plus the expenditures of RINs. As a note, we did not include the perceived cost of the RFS from the potential damage to engines from increased ethanol consumption, as there is only limited information quantifying this effect.

In our estimate of increased ethanol consumption owing to the RFS, it is also possible to estimate the potential GHG emission decrease, or increase attributable to the RFS, based on research from Argonne National Laboratory (ANL) and a study published in the Proceedings of the National Academies of Sciences. When these emission estimates are combined with our cost estimates, we are also able to calculate the potential abatement cost of the RFS as a climate-improving program.

Results

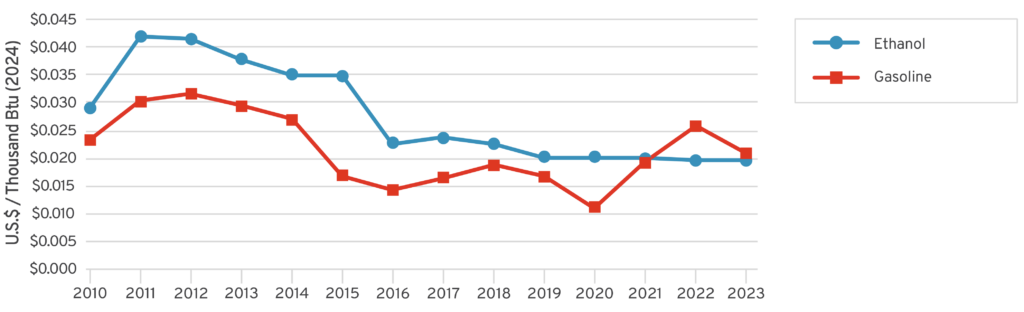

Figure 1 shows that ethanol is, on average, more expensive per unit of energy than gasoline, which is not surprising given ethanol’s lower energy density as well as its elevated demand resulting from the RFS mandate. Except for years 2022 and 2023, where refinery capacity scarcity elevated gasoline prices, ethanol was always more expensive in our assessed time period than gasoline. However, this price difference was fairly narrow, which we expected, given the limited substitutability of the fuels (i.e., if the price of one type of fuel were to go up, we would expect demand to shift to the other type of fuel, which induces pricing equilibrium).

Figure 1: Energy Cost of Liquid Fuel

Source: R Street calculations based on U.S. EIA fuel costs and production data available at https://www.eia.gov/totalenergy/data/browser. Last accessed May 31, 2025.

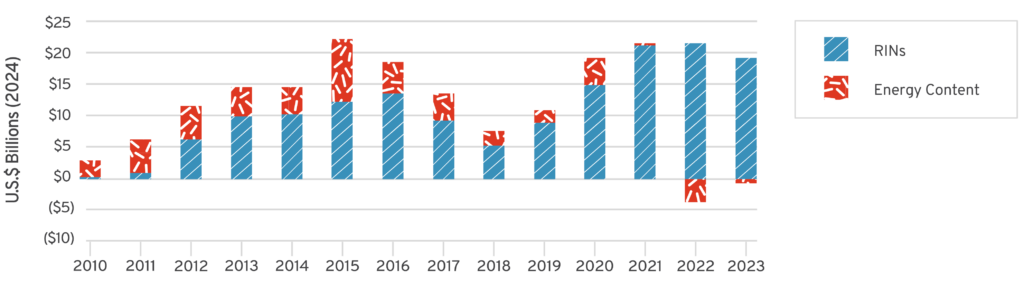

We then calculated how much additional ethanol was consumed as a result of the RFS. We estimated this to be approximately 7.8 quadrillion British thermal units (Btu) from 2010 to 2023, or about 89 percent higher than our no-RFS scenario. In estimating the cost difference of purchasing this energy as ethanol rather than gasoline and adding the expenditures for RINs, we can then estimate a total consumer cost of the RFS, which is shown in Figure 2.

Figure 2: Consumer Cost of the RFS

Our analysis shows that the additional ethanol consumed to comply with the RFS from 2010 to 2023 (i.e., the amount consumed beyond our baseline assumption that finished motor gasoline would contain 5 percent ethanol if the RFS had not been implemented) cost $214.5 billion, and purchasing this same energy as gasoline would have cost $168.5 billion, for a difference of $46 billion. If narrowing this timeframe to a standard 10-year analysis window from 2014 to 2023, the cost difference would be $28.1 billion.

We also calculated that, given the cost of conventional biofuel RINs, approximately $152.8 billion was expended for RFS compliance from 2010 to 2023, representing a cost that refiners pass on to consumers in the form of higher pump prices. If narrowing this timeframe to a standard 10-year analysis window, from 2014 to 2023, $135.8 billion was expended. Thus, overall, we found that the combined increased cost of energy and compliance to consumers from 2010 to 2023 was $198.9 billion, or $163.8 billion from a 10-year analysis window of 2014 to 2023. It should be noted, though, that as more recent data becomes available, this 10-year cost would likely fall, as RIN prices—which reflect the majority of the RFS’ cost—have fallen considerably recently.

An additional research question our analysis sought to answer was whether the wholesale price of ethanol incorporated the cost of RINs, meaning whether the compliance cost of the RFS was absorbed by ethanol refiners or passed through to ethanol buyers. Our research found that in the past, ethanol refiners were likely accounting for the cost of RFS compliance in ethanol wholesale prices, as the cost of ethanol was higher per unit of energy relative to gasoline, but the cost of RINs was very low. In more recent years, we saw the opposite, with RIN costs rising and accounting for most of the RFS cost and the cost of ethanol relative to gasoline being lower. Simply put, ethanol refiners are likely able to use the value of RINs to subsidize the cost of ethanol. From an economics perspective, this indicates a distortion where the artificial market created by the RFS forces consumers to pay a higher cost that does not reflect any additional value from ethanol consumption.

Emission Impact

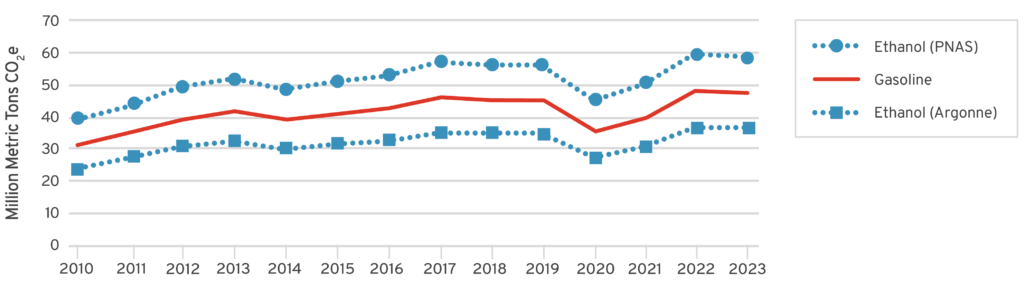

One of the primary justifications for the RFS in the 2007 Energy Independence and Security Act was to lower GHG emissions. The RFS requires (and the EPA affirms) that ethanol has 20 percent lower GHG emissions per unit of energy than gasoline, and, therefore, that the mandate of additional ethanol consumption to supplant gasoline lowers transportation emissions. However, more recent research calls that assumption into question, demonstrating a wide range of estimates of potential emission declines, with some even showing an increase in emissions associated with ethanol consumption.

For example, the ANL’s GREET model estimates that conventional corn-based ethanol has 40 percent lower lifecycle emissions than gasoline. In contrast, a recent study published by the Proceedings of the National Academies of Sciences estimated that ethanol emits 24 percent more GHG than gasoline. These estimates are so far apart because they are based in part on assumptions of alternative uses for land that is utilized for corn production to meet RFS demand. If one assumes that farmers would be using the land anyway for other crops, then ethanol can have lower lifecycle emissions than gasoline. If, however, one assumes that the RFS has resulted in more land being transitioned from non-agricultural use into agricultural use, then lifecycle ethanol emissions would be higher. Figure 3 demonstrates the range of emission abatement (or increase) relative to gasoline that could be attributed to the RFS using our assumption of a 5 percent blend rate without the program.

Figure 3: Emissions of Additional Ethanol Consumption via the RFS

Source: R Street calculations based on U.S. EIA fuel costs and production data available at https://www.eia.gov/totalenergy/data/browser. Last accessed May 31, 2025.

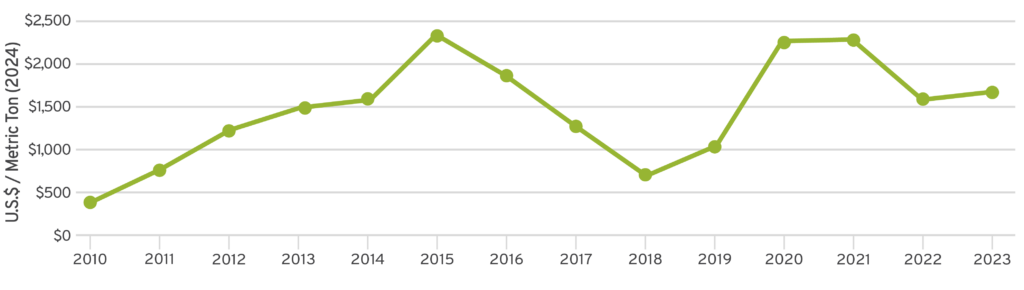

Additionally, we estimated the abatement cost of the RFS. We conservatively applied the assumption that ethanol has lower emissions than gasoline and also applied ANL’s more favorable finding of ethanol having 40 percent lower emissions than gasoline. In so doing, we calculated that the abatement cost per metric ton of carbon dioxide emissions is, on average, $1,464.27, about 75 percent of which is from the cost of RINs. However, the abatement cost varies substantially, depending on the cost of ethanol as well as RFS RINs in any given year. Figure 4 shows the abatement cost of the RFS from 2010 to 2023.

Figure 4: Abatement Cost of the RFS

Source: R Street calculations based on U.S. EIA fuel costs and production data available at https://www.eia.gov/totalenergy/data/browser. Last accessed May 31, 2025.

Overall, our calculations suggest that the RFS is an inefficient emission abatement tool that costs notably more than alternative abatement policies. While one could assert that even high-cost climate policies are worthwhile, it is important to note that the highest estimated social cost of carbon was during the Biden administration, at $190 per metric ton, which is significantly lower than the abatement cost of the RFS. Ultimately, this means that the RFS is not cost-effective as a climate policy.

Discussion and Policy Recommendations

The RFS was initially justified to address U.S. energy security and reduce GHG emissions. Concerns about its potential cost have been dismissed, owing to expectations that the mandates varied little from anticipated ethanol consumption. However, historical ethanol consumption before the adoption of the RFS was well below current rates of ethanol blending, and other regions of the world with high gasoline prices have not relied on biofuels to the same extent as the United States. This suggests that the RFS is artificially increasing ethanol consumption and thus increasing costs to fuel consumers owing to its higher cost.

In our analysis of the RFS using reasonable fiscal assumptions, it became clear that the program incurs a considerable cost to consumers—$163.8 billion over a standard 10-year analysis period—indicating that the program may need further scrutiny.

Additionally, to justify the program, we should be able to demonstrate that comparable benefits are achieved from both its energy security and climate goals. However, the energy policy landscape on both fronts has changed considerably since the RFS’s inception. From an energy security perspective, the United States’ considerable increase in oil production since the RFS’s initial drafting lessens the potential benefits of the program. Instead of displacing foreign sources of energy, the RFS is more likely to displace domestic ones. Furthermore, from a climate perspective, even when utilizing favorable assumptions, the RFS’s potential abatement cost far exceeds the social benefit from avoided climate change.

Ultimately, our analysis led us to conclude that, in the current energy landscape, there is minimal economic, environmental, or national security justification for the RFS. Defendants of the RFS will likely argue that our assumption of ethanol consumption absent the RFS is too low, but even if that is the case, we contend that the RFS should still be repealed so that the market—rather than politicians—can determine the optimal level of ethanol-gasoline blending.

Conclusion

The RFS was initially envisioned as a means of delivering energy security and climate benefits at a low cost. However, our analysis shows that the cost of the program likely exceeds its benefits. This is due to both the rising costs of the RFS as well as the nation’s reduced reliance on foreign oil supplies over the last 20 years. Additionally, the potential climate benefits of the RFS have been cast into doubt, as recent research has exposed uncertainty regarding the GHG emission improvements of ethanol over gasoline. Given the RFS’ high cost and lessened justification, policymakers should repeal it.