What you would have made if you bought big lenders in 2006

Suppose you had decided at the end of 2006, when it looked like lending businesses were booming, to invest $10,000 equally divided among the common stock of the dozen biggest U.S. lending institutions. Those would have been eight bank holding companies, two thrift holding companies and two government-sponsored enterprises. Specifically, ranked by total assets, that would have been: Citigroup, Bank of America, JPMorgan, Fannie Mae, Freddie Mac, Wachovia, Wells Fargo, Washington Mutual, U.S. Bancorp, Countrywide Financial, SunTrust and National City.

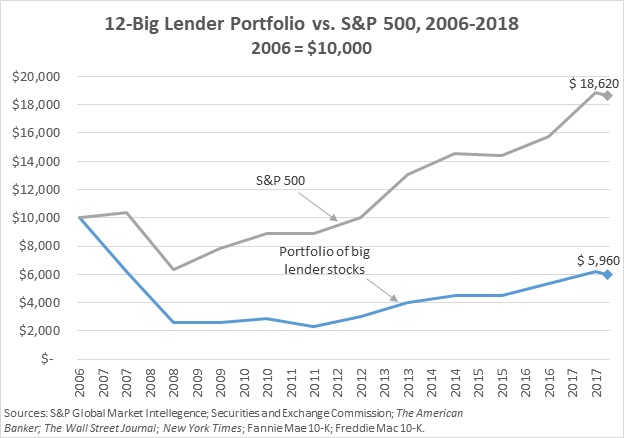

How would you have done? Your portfolio, bought for $10,000, would at the end of March 2018, eleven years later, been worth $5,960. You would be still be down more than 40 percent. Of course, you are now better off than at the bottom of the stock market in 2009, when it was worth $2,569, or down 74 percent. But the more than eight years since have not gotten you back to even, far from it. The unfortunate history of your big lender portfolio is shown in the following table.

You are also in poor shape relative to the Standard & Poor’s 500 index. As of March 2018, you are about 68 percent behind the alternative of having put your $10,000 in the S&P. Your current $5,960 compares to the index’s current $18,620. The history of the relationship is shown in the following graph.

Of course, the performance over the whole period of the lenders’ individual stocks varies by a lot. From the virtually 100 percent loss in Washington Mutual, to the 98 percent losses in Fannie and Freddie, to the 88 percent loss in Citigroup and 44 percent loss in Bank of America, we find gains of 47 percent in Wells Fargo and 128 percent in JPMorgan. Overall, there are nine institutions with their value still down after more than 11 years and only three that are up versus 2006.

It is true that financial markets are always energetically looking forward with thousands of eyes, minds and computers. But despite the diligent efforts, they often don’t see forward very well. So indeed it was in 2006, with the stock prices of the biggest lending institutions at the top of the first (and assuredly not the last) great 21st century bubble.