Reassessing Scope 3 and Emissions Disclosure Policy

State-law requirements for businesses to disclose greenhouse gas (GHG) emissions are expanding. California, for example, requires large companies doing business in the state to report not only their direct operational emissions, Scopes 1 and 2, but also Scope 3 emissions, which are the indirect emissions embedded across product supply chains. Beyond California, New York, New Jersey, Illinois, Washington, and Colorado have proposed similar policies. Collectively, these states account for more than a third of U.S. economic output, indicating the potential for a substantial portion of U.S. economic activity to fall under emission disclosure requirements. In this context, policymakers should have better information as to the costs and benefits of such policies, as well as the limitations of expanded disclosure.

The Role of the Greenhouse Gas Protocol in Disclosure Mandates

The Greenhouse Gas Protocol (GHGP) is the dominant corporate emissions accounting framework, and its widespread usage facilitates state-driven disclosure policies. The underlying logic behind disclosure requirements is straightforward: If climate risk is systemic, then disclosure should be systemic as well. A complete disclosure of emissions, however, necessitates an increased reliance on measuring Scope 3 emissions, which can raise new challenges for firms.

On average, Scope 3 accounts for roughly 75 percent of a company’s total emissions on average, and some analyses place that figure closer to 90 percent. In certain sectors such as manufacturing, retail, and materials, Scope 3 emissions can be many times larger than combined Scopes 1 and 2. From this perspective, focusing only on direct emissions offers a narrow view of the climate exposure embedded in supply chains and product use. Investors concerned about the potential costs of policies that mandate emission reductions (called “transition risk”) understandably want visibility into that larger picture.

But expanding disclosure is not costless, and coverage is not synonymous with clarity. A workable disclosure regime must produce reliable, decision useful information at a reasonable cost. Current Scope 3 mandates struggle to meet that standard.

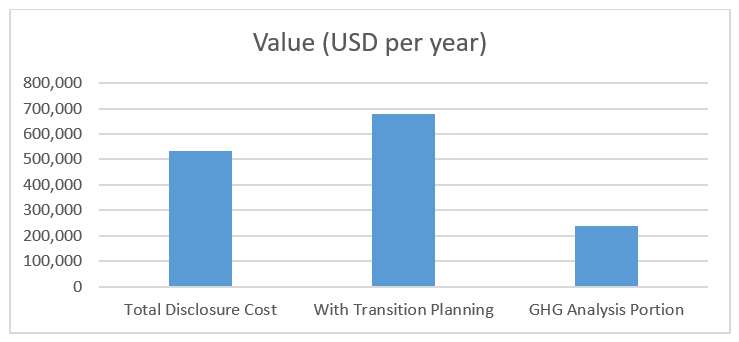

Compliance with Scope 3 reporting, however, is difficult and expensive. Scopes 1 and 2 can generally be measured through fuel consumption and purchased electricity, but Scope 3 requires collecting data from upstream suppliers, modeling downstream product emissions, and relying on emission factors and assumptions, such as average industry emission factors, consumer usage patterns, product lifetimes, and energy grid mixes. Collectively, these requirements push the average annual cost of climate related disclosure compliance per company to approximately $533,000. When voluntary transition planning activities—such as developing net-zero roadmaps, conducting scenario analysis, and creating climate transition plans—are included, that figure rises to $677,000. Of the full $677,000, roughly $237,000 is devoted specifically to greenhouse gas analysis and disclosures, an area heavily driven by Scope 3 estimation and reporting requirements. For smaller companies, these recurring expenses can represent a significant share of their operating budgets.

Source: ERM

Investors face costs as well. Institutional investors spend an average of $1.37 million annually on climate data analysis and reporting, including substantial expenditures on Environmental, Social, and Governance (ESG) ratings. While those costs are distributed across portfolios, they reflect the broader system-wide commitment of capital and labor to maintaining the Scope 3 reporting architecture. In aggregate, disclosure mandates redirect significant resources toward estimation, auditing and reporting infrastructure. That investment may be justified if it materially improves capital allocation or accelerates emissions reductions. If not, the opportunity cost becomes harder to defend.

Source: ISS

Challenges in Scope 3 Estimation

The tension between Scope 3 data collection costs and its value lies in the nature of the data itself. Small methodological changes can produce large swings in reported totals, even if underlying operations remain unchanged. This is because Scope 3 disclosures often rely on modeled estimates instead of direct measurements. Although emissions from a company’s suppliers can be approximated using industry averages, accurately estimating these downstream emissions from a product’s use requires assumptions about consumer behavior, product lifetimes, and usage patterns. This introduces comparability challenges across firms and volatility over time. Two companies in the same sector may report completely different Scope 3 emissions not because of performance differences but because they estimate their emissions differently. The same emissions can be counted multiple times across firms, appearing as Scope 1 for one firm and Scope 3 for another. Although accounting frameworks attempt to manage this overlap, the aggregation of estimates across the economy can obscure rather than clarify responsibility.

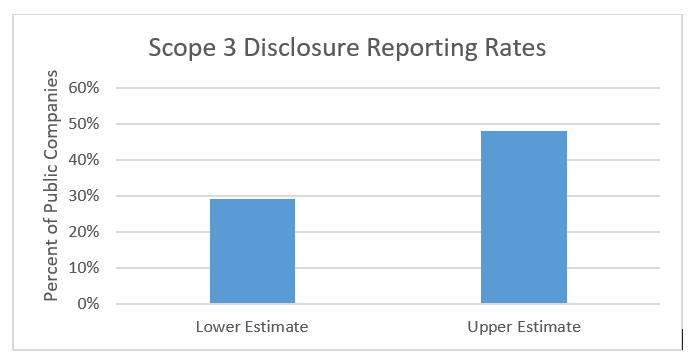

Reporting rates reflect these difficulties. Estimates suggest that only 29 to 48 percent of public companies fully disclose Scope 3 emissions. Even among those that do, methodologies vary widely, leaving investors with broader coverage but uneven precision. The result is a regime that dramatically expands emissions visibility while delivering data that can be difficult to interpret with confidence.

None of this means Scope 3 emissions are irrelevant. On the contrary, value chain emissions matter for understanding transition risk and long-term strategy. Many firms voluntarily measure Scope 3 emissions and report internal benefits such as improved supplier engagement and enhanced risk awareness.

Reforming Scope 3 Mandates

The problem is not the concept of Scope 3 itself, but the rigidity and breadth of current mandates. Converting a private management tool into a universal legal obligation raises the stakes. When compliance becomes compulsory, regulators must ensure that the resulting information is sufficiently reliable and useful to justify recurring six figure costs (or higher) per firm.

A more effective path forward would focus less on expanding categories and more on improving precision. Rather than requiring disclosure of every conceivable downstream scenario, policymakers could prioritize emission categories that are demonstrably material and reasonably measurable. Establishing clearer materiality thresholds and safe harbors for estimation methodologies would reduce compliance uncertainty while preserving transparency. Narrowing mandatory categories to the most decision relevant components of Scope 3 would align reporting obligations more closely with investor needs.

At the same time, policymakers should create space for innovation in product level carbon accounting. Ledger based systems and product carbon footprint methodologies assign emissions to specific goods or services and transmit that information along supply chains. By treating emissions more like financial attributes attached to transactions, these systems reduce double counting and enhance traceability of embedded emissions. Buyers can compare products based on carbon intensity, and suppliers can compete on measurable performance. Such approaches align more closely with financial accounting norms of single counting, verifiability and auditability. Allowing product level reporting as a compliance alternative to broad corporate Scope 3 aggregation would encourage experimentation with more precise, verifiable accounting methods while maintaining transparency goals.

A solutions-oriented framework would also subject disclosure mandates to rigorous cost benefit analysis. Policymakers should ask whether Scope 3 data materially affects capital flows, credit pricing or corporate investment decisions. If evidence of decision usefulness is limited, reporting requirements should be recalibrated. Measuring incremental emissions reductions attributable to disclosure, comparing compliance costs with climate risk mitigation benefits and evaluating alternative policy tools would ground climate disclosure policy in the same analytical standards applied to other economic regulations.

Toward More Effective Climate Disclosure

Climate policy does not operate in isolation from economic growth. Half a million dollars per year in compliance cost may be manageable for the largest multinational corporations, but it is not trivial for smaller public companies or firms considering public listing. Furthermore, these disclosure burdens may vary among firms, and deter businesses from engaging in activities that may complicate their disclosure frameworks. Resources devoted to consultants and reporting systems are resources not invested in operational improvements, capital upgrades or research and development that could directly reduce emissions. An optimized disclosure framework should maximize emissions reductions per dollar of compliance spending.

Reframing the Scope 3 debate as an optimization problem rather than an ideological one opens the door to constructive reform. The objective is not to abandon transparency, nor to ignore value chain emissions. It is to ensure that disclosure mandates produce reliable signals that markets can use. Precision, comparability and proportionality should guide policy design.

Scope 3 emissions will remain central to climate risk discussions. But the durability of disclosure policy depends on its economic credibility. When mandates impose substantial costs yet produce highly variable data, skepticism is predictable. A smarter path emphasizes refinement over expansion and quality over quantity. Climate transparency should illuminate risk, not multiply paperwork.