Carbon Dioxide Removal Will Face Mixed Permitting Challenges

Introduction

There is a burgeoning demand for carbon dioxide removal (CDR), and the technology is playing an increasingly critical role in net-zero emission scenarios. To date, there are very few CDR facilities, and this is despite the existence of expanded subsidies and private investment. But the CDR industry has considerable growth expectations, and this growth may trigger substantial permitting challenges that constrain CDR expansion. Recent R Street analysis found that permitting restrictions on clean energy are increasing rather than decreasing. Importantly, these findings are consistent with research showing that, despite its general popularity, clean energy faces just as much local opposition to infrastructure development as other resources.

This piece examines CDR, highlights expected permitting challenges, and acknowledges where some CDR aspects may have easier permitting pathways.

CDR Permitting Concerns

Direct Air Capture

Permitting issues depend upon the method of CDR used. The most discussed form of CDR is direct air capture (DAC) which involves reacting atmosphere with chemicals to separate carbon dioxide (CO2). Because this method has the same effectiveness regardless of location, it can be sited in areas where permitting constraints are minimal. Additionally, because DAC typically uses chemicals in a closed-loop process, it may prevent discharge into bodies of water and avoid permitting delays via Clean Water Act (CWA) permits. However, if the goal of DAC is to utilize pipelines in its sequestration of CO2, it may encounter challenges in pipeline permitting. Fortunately, siting DAC near existing CO2 pipelines can mitigate these challenges.

Ocean-Based Capture

Ocean-based CDR is more likely to encounter permitting difficulties than DAC. There are several forms of ocean-based CDR with varying levels of impact. Specifically, direct ocean capture (DOC), which removes CO2 from seawater, requires coastal infrastructure while artificial upwelling and downwelling CDR methods may require offshore physical infrastructure. Local permitting on coastline is already likely to be more complex than permitting in areas that are less disruptive to nature, but there are some specific permitting challenges where water is concerned.

The first is that DOC technology, by its nature, requires water intake—meaning that states may have to issue permits under Section 316 of the CWA. If states are unwilling to issue these permits, projects could be delayed indefinitely. To the extent that regulators may be uninformed or have extraordinary concerns regarding novel technologies like DOC, issuance of CWA permits may be delayed.

Additionally, coastal or offshore CDR requires additional permitting. Principally, leases must be issued for those activities, and acquiring such leases may be difficult. While there are processes in place for leasing offshore areas for oil and gas activity, there is no corollary process for CDR. At least in the case of oil and gas, the federal government has been exceptionally restrictive in its issuance of offshore leases. Furthermore, because the issuance of a lease for CDR could be construed as a major federal action, ocean-based CDR will likely require review under the National Environmental Policy Act (NEPA). Should such projects require an environmental impact statement (EIS) under NEPA, they will reckon with the issue that EISs take an average of 4.5 years to complete. Importantly, clean energy-related technologies are more likely to require EIS review than other energy types. An R Street analysis found that 90 percent of energy-related projects listed on the Federal Permitting Dashboard were clean energy-related.

Other Forms of CDR

Other methods of removing CO2 from the atmosphere—such as afforestation, soil sequestration, or biomass carbon removal—typically rely on some natural element. While permitting challenges come into play to a certain extent for these carbon-removal methods because of their relative land-intensity compared to DAC or DOC, they largely rely on turning existing permitted activities (like agricultural production) into carbon-removal opportunities. While it is important to acknowledge that permitting challenges remain for these forms of CDR, they are more likely to encounter commercialization challenges in the form of difficulties in measurement, reporting, and verification standards.

CO2 Pipelines

While CO2 pipelines are not a direct component of CDR, some forms of CDR require CO2 pipelines to transport removed CO2 to an endpoint for storage or utilization. The need for CO2 pipelines can be minimized to a certain extent by siting CDR near the CO2’s intended destination—for example, building DAC as close as possible to their geologic storage sites or pipeline access points. But achieving large-scale CDR is likely to require considerable CO2 utilization in activities like enhanced oil recovery (EOR) to recoup financial costs.

Getting CO2 to end-use customers will almost certainly require additional pipeline infrastructure. Ironically, while pipeline permitting is an exceptionally complicated issue for oil and gas, it is even more complicated for CO2 despite its role in the public interest.

The authority for permitting pipelines varies by type, with natural gas pipelines largely under the purview of the Federal Energy Regulatory Commission (FERC) and oil pipelines under state authorities. Pipelines are also subject to regulation by the U.S. Pipeline and Hazardous Materials Safety Administration. CO2 pipelines, though, are in a difficult spot in terms of permitting. Because the court decision in Exxon Corp. v. Lujan determined that Mineral Leasing Act (MLA) requirements for “natural gas” pipelines also extend to naturally occurring gases, CO2 must comply with more stringent regulation—even if what is transported via pipeline is anthropogenic in nature.

Further complicating this issue is the fact that, despite CO2 being classified as a natural gas for the purpose of the MLA, FERC does not undertake authority for the permitting of these pipelines because CO2 is not considered energy. Even though they have applications in the energy industry, CO2 pipelines— unlike conventional natural gas (methane) pipelines—do not have easy access to eminent domain or other procedures that can aid in the land assemblage required for a pipeline corridor.

Essentially, CO2 pipelines are regulated by states, and each state may have different regulations for how CO2 pipelines may be built and operated. A simple inference is that it will be easy to build CO2 in some states and more difficult in others. This is true prima facie, and we do see states like California and Illinois explicitly imposing state-level moratoria on CO2 pipelines—proving a heterogeneous permitting environment across the nation. However, even in states where it should presumably be easier to permit CO2 pipelines, difficulties remain.

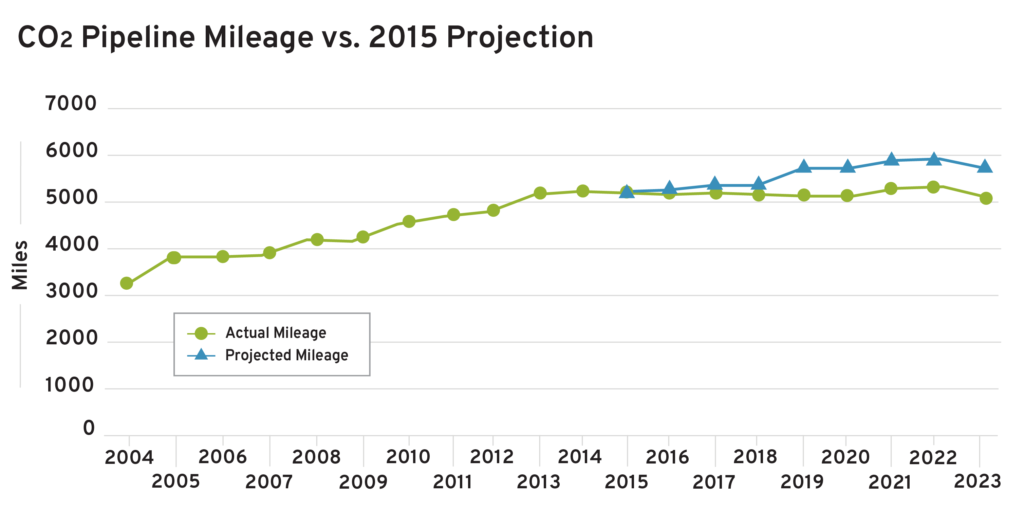

There are currently approximately 5,000 miles of CO2 pipelines in the United States, most of which are in the Permian Basin. Most of these pipeline miles were constructed from 1980 to 1990, with CO2 pipeline construction slowing down considerably in the ‘90s despite the Section 43 tax credit available for EOR at the time. According to a 2024 analysis, it will take between 20,000 and 96,000 miles of CO2 pipelines to achieve carbon neutrality in the United States by 2050—though these estimates are slightly more conservative than a 2008 estimate of up to 120,000 miles. A 2015 National Energy Technology Laboratory (NETL) analysis anticipated modest pipeline growth, with 10 CO2 pipeline projects planned to come online before 2020, adding over 500 miles of pipeline. However, as of 2023, the total mileage of CO2 pipelines has slightly decreased.

Sources: Pipeline and Hazardous Materials Safety Administration and NETL Analysis

Additionally, a Congressional Research Service report has found that of the four large CO2 pipelines in development since 2021, none have been able to secure a permit, with three of the four being denied siting permits. The fourth is a conversion of an existing natural gas pipeline, and whether state authorities will issue a permit once it leaves FERC’s jurisdiction is yet to be determined.

Quite simply, it is very difficult to permit CO2 pipelines at the state level; there is no effective federal permitting authority yet; and CO2 pipeline construction has stalled despite the availability of subsidies for end-use and sequestration via 45Q tax credits and private-sector interest in carbon capture, utilization, and storage (CCUS).

Carbon Sequestration Wells

CDR that aims to geologically sequester CO2 will encounter permitting hurdles in two forms: Class VI carbon sequestration wells and Class II enhanced recovery wells. The U.S. Environmental Protection Agency (EPA) has the primary authority for permitting wells of all types in the United States, but given the impracticality of the EPA having to permit so many wells, it cedes its permitting authority to states in circumstances where state regulators can ensure adequate or better compliance and environmental outcomes. For Class II wells used for EOR, essentially every state that has EOR also has primacy. For Class VI wells, though, only three states have primacy: Louisiana, North Dakota, and Wyoming.

Source: U.S. Geological Survey CO2 Sequestration Potential Map

While EOR has focused mainly on the Permian Basin, a region that already has robust oil and gas infrastructure, geologic sequestration of CO2 is most feasible in Texas, the Gulf Coast, and the East Coast. The Pacific Northwest and some parts of the Western United States and Alaska also have great potential for geologic sequestration. However, many of these regions have little experience with pipelines and wells and may struggle to develop regulatory regimes for such industries—if they engage in the activity at all.

The fact that the federal government has primacy for Class VI wells in most of the country is partially a problem because they take longer to permit wells than state governments do. For instance, it takes the federal government 94 days to approve a drilling permit compared to 23 days in Texas. A larger issue is the disconnect wherein both states and the federal government have opportunities to delay or deny projects: The federal government can deny well permits, while state governments can deny pipelines to the wells. This makes it more difficult for businesses trying to sequester wells to have confidence in reasonably quick and certain permitting.

Policy Implications and Recommendations

Past R Street research has found that, in general, newer technologies are more likely to get snarled in permitting challenges. This is partially because legacy technologies like oil and gas have received categorical exclusions (CXs) via legislation, but also because those technology types are well understood, and institutions have a long history of permitting them. The institutional knowledge does not yet exist for CDR and supporting infrastructure like CO2 pipelines, but permitting challenges are likely to pose a major barrier to the market entry of new technologies.

The scope of permitting challenge will depend almost entirely upon the scale of the project and its likelihood to disrupt local communities and habitat. To this extent, permitting risks are greatest for ocean-based CDR and supporting CO2 pipelines and less of a concern for DAC or CDR that relies on adjusting practices in agriculture or forestry. While more comprehensive recommendations for ocean-based CDR and CO2 pipelines exist, we recommend several near-term priorities for policymakers on CDR and permitting.

1. Consistently apply existing CXs across technology types

To the extent that ocean-based CDR, pipelines, or CO2 sequestration wells rely on technology used in the oil-and-gas sector, existing CXs should be expanded to include CDR and CCUS-related projects. As a note, R Street has cautioned against technology-specific carve-outs for CXs because they can distort markets. For this reason, CXs should focus on well-understood technology to accelerate permitting that requires NEPA compliance.

2. Consider clarifying the MLA to focus on natural gases combusted for energy

The Exxon Corp. v. Lujan decision, now more than 30 years past, seems out of place. The common understanding of natural gas is methane used as a hydrocarbon fuel, and the MLA ensures that leases for such fuels return adequate economic value. Presently, however, the sequestration of CO2 is primarily pursued as a public good rather than to yield a private benefit—meaning the MLA sets too high a bar for approving CO2 pipelines. The court decision made sense at the time because even though the pipeline in question transported mostly CO2, it still transported significant quantities of methane. Modern CO2 pipeline debates focus on pipelines transporting CO2 almost exclusively. Congress must clarify the requirements for CO2 pipelines under the MLA.

3. Ensure ocean-based CDR has a pathway to securing necessary leases

One major challenge with offshore leasing is the inordinate level to which the process is subjected to political preferences. The Inflation Reduction Act explicitly required the administration to resume offshore energy leases for oil and gas, but the offered leases constituted only the bare minimum (three as opposed to the normal 20). If it can be approved, ocean-based CDR may have more economic potential than other forms of CDR. But because coastal and offshore infrastructure is likely to require federal permits, it will need a clear process for attainment.

The 2021 Bipartisan Infrastructure Law directs the Bureau of Ocean Energy Management to do exactly this, but ocean-based CDR is in limbo until a final determination is produced. Even after a process is created, there is no guarantee it will not need further reform or intervention from future legislation to ensure market access.

Additionally, Congress should clarify to what extent states may withhold the issuance of permits under the CWA to avoid situations where infrastructure that complies with all necessary environmental requirements is prevented by state-level political opposition.

4. Expand Class VI well-permitting primacy to states with CO2 sequestration potential

This ought to be a priority because even though states must develop their own permitting protocols for Class VI wells to be eligible for primacy, they are typically faster to issue permits and more likely to understand what localized risks to address in permitting decisions. Retention of EPA authority over sequestration well permitting is likely to make CO2 storage more difficult in the long term.

Conclusion

While the concept of CDR in and of itself ought not to present exceptional permitting challenges, its tangential interaction with difficult-to-permit infrastructure like pipelines, coastal, and offshore infrastructure make it vulnerable to permitting delays and disapprovals. Importantly, the types of permits required are notoriously vulnerable to politicization and delays.

The good news is that many challenges are addressable through relatively modest adjustments to permitting policy. In the case of CO2 pipelines especially, much of the need is simply for Congress to define how CO2 is considered in the regulatory sphere of energy-related gases that are transported. Congress can also direct federal agencies involved in coastal and offshore permitting to establish guidelines for permitting of CDR-related infrastructure.