Debt and National Security Part 1: Borrowing Away Military Flexibility

Debt is not inherently bad. Governments often borrow to finance wars, recessions, pandemics, and other emergencies that require immediate resources. In many ways, borrowing is simply a way of shifting resources across time, using future income to meet present needs. The problem arises when emergency-level borrowing becomes permanent rather than temporary. This creates a national security challenge by limiting the government’s ability to respond to future threats.

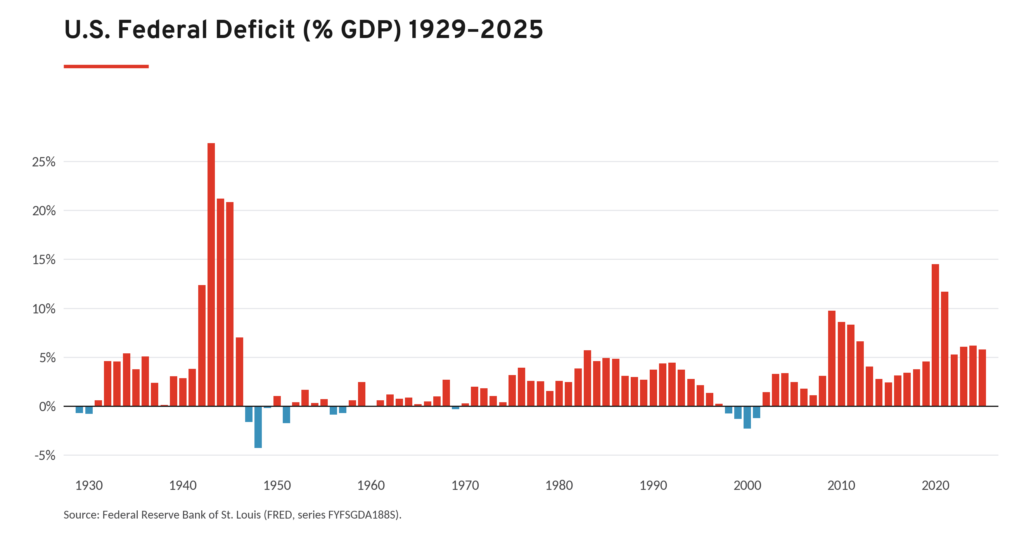

The idea rests on a simple principle: solvency. A government is solvent if its future fiscal capacity is sufficient to service its debt obligations. Historically, the United States has generally followed this pattern. The following chart shows federal deficits as a percentage of gross domestic product (GDP) from 1929 to 2025. Deficits rose sharply during major crises including World War II, the Cold War buildup of the 1980s, the Great Recession, and the COVID-19 pandemic. In these instances, the government required immediate fiscal resources to respond to extraordinary circumstances.

What happened in the aftermath of those crises is crucial. Fiscal consolidation typically followed periods of elevated deficits, allowing debt growth to stabilize over time. Today’s situation looks different. Since 2022, federal deficits have remained around 6 percent of GDP despite the absence of a comparable national emergency. The last federal budget surplus occurred in 2001. In other words, emergency-level borrowing has increasingly become a permanent feature of fiscal policy.

Fiscal health requires more than solvency. It also requires liquidity—the ability to meet current obligations in full and on time. Just as households must make interest payments on their loans, governments must make interest payments on their debt. The larger the debt stock becomes, the more resources must be devoted to servicing past borrowing rather than meeting present needs.

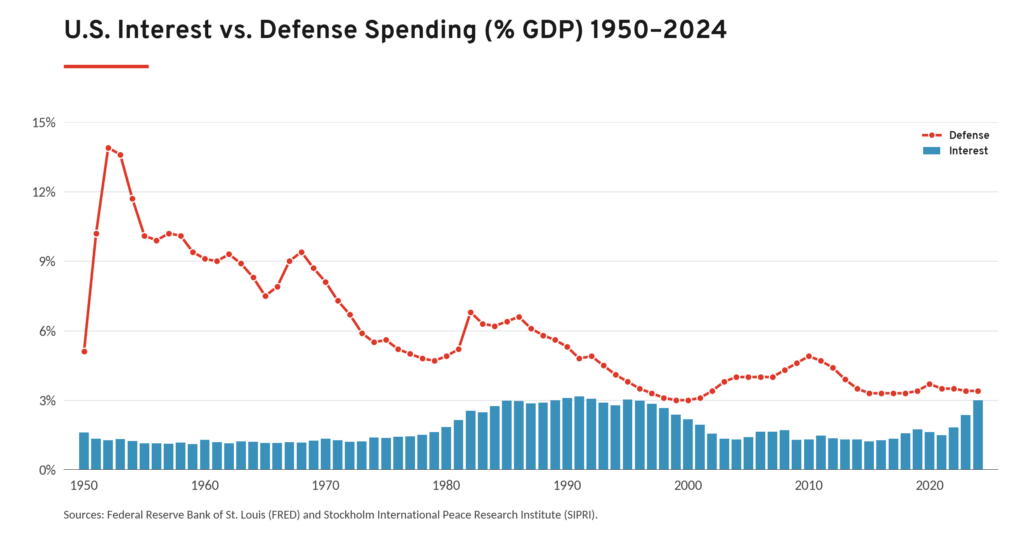

The following chart compares federal interest payments and defense spending as shares of GDP beginning in 1950. In 2024, the United States spent approximately 3.00 percent of GDP on net interest payments and 3.43 percent of GDP on defense. For every dollar devoted to national defense, the government spent approximately 87 cents servicing accumulated debt. Interest payments have become one of the largest categories of federal spending, trailing only Social Security.

This trend matters because interest payments do not purchase aircraft carriers, train soldiers, strengthen alliances, modernize infrastructure, or invest in other sources of national power. They merely compensate past borrowing. As interest costs rise, policymakers face increasingly difficult trade-offs between servicing debt and funding current priorities.

Moreover, interest costs are projected to continue increasing steeply. In the first eight months of Fiscal Year 2026, interest costs have risen 8.8 percent compared to the previous year. This level of spending on interest is comparable to the 1980s and 1990s. However, unlike the high-interest-rate environment of the 1980s, when the Federal Funds Effective Rate reached almost 20 percent, today’s interest burden is occurring despite a substantially lower effective rate of 3.64 percent and lower defense spending as a share of GDP. This suggests that the sheer size of the accumulated federal debt—rather than unusually expensive borrowing—is the primary driver.

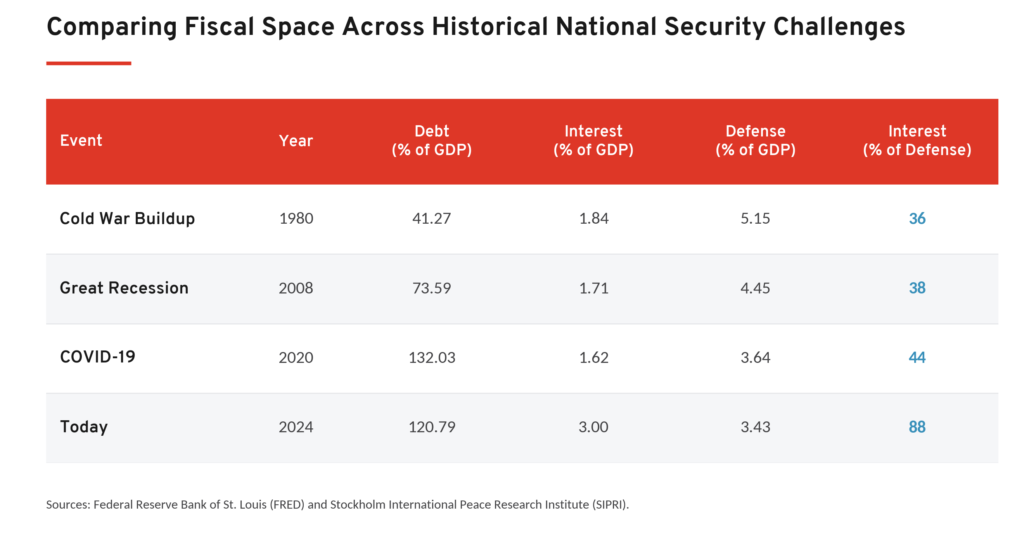

To illustrate this growing constraint, the following table introduces a simple measure I call the “Fiscal Space Index”: the ratio of interest payments to defense spending. A higher value indicates that a larger share of national resources is being devoted to servicing past debt relative to improving military capability.

The results are striking. Interest payments were roughly 36 percent of defense spending during the Cold War buildup of 1980, increasing to 38 percent during the Great Recession, and 44 percent during the COVID-19 pandemic. By 2024, interest payments had risen to nearly 88 percent of defense spending—an all-time high for the period examined.

The national-security implications are difficult to ignore. As one pillar of national security, military strength ultimately depends on economic capacity. A government that devotes an increasing share of its resources to debt service has fewer resources available for defense, diplomacy, technological investment, and crisis response.

Just as importantly, high debt reduces strategic flexibility. Over the past two decades, the United States has repeatedly faced unexpected crises—from financial collapse to global pandemics and growing geopolitical tensions in Europe, the Middle East, and Taiwan. Responding effectively to future challenges could require substantial fiscal resources, and every year of elevated deficits and rising interest payments reduces the government’s room to maneuver.

National security begins with fiscal capacity. A nation that enters future crises with record debt and rapidly growing interest obligations has less flexibility than one with a strong fiscal foundation. By that measure, federal debt is not merely an economic concern. It is increasingly a threat to national security.