What have the massive guarantees of mortgages by the U.S. government achieved?

This study originally appeared in the Winter 2017 edition of Housing Finance International.

Author

Study

The U.S. government, through multiple agencies, indulges in massive guarantees of U.S residential mortgages. Much, but not all, of this happens through the formerly celebrated, then failed, humiliated and notorious, Fannie Mae and Freddie Mac. These companies, now owned principally by the U.S. Treasury and completely controlled by the government as conservator, are still mammoth, with $5 trillion in combined assets. And there are trillions of dollars of additional government involvement in the U.S. housing finance sector, which with $10.4 trillion in outstanding rst lien loans, is the largest loan market in the world.

In the early 2000s, in the days B.B.B. [Before the Bursting Bubble], I had the pleasure to meet in Copenhagen with representatives of the Danish Mortgage Banking Association. They presented their highly interesting, efficient and private mortgage bond-based housing finance system, and I presented the government-centric, Fannie and Freddie-based mortgage system of the United States. (I was describing, by no means promoting, this system.) When I had finished my talk, the chief executive of one of the Danish mortgage banks made this unforgettable observation, “You know, in Denmark we always say that we are the socialists and America is the land of free enterprise and free markets. But I see that in housing finance, it is just the opposite!”

He was so right.

What has all the U.S. government intervention in mortgage credit achieved, if anything?

In 1967, the U.S. home ownership rate was 63.6 percent. Today, in 2017, it is 63.7 percent. After fifty years of intense government mortgage credit promotion and guarantees, the home ownership rate is just the same as it was before. The government mountain labored mightily and brought forth less than a mouse, at least as far as the home ownership rate goes.

The scale of the U.S. government’s absorption of mortgage credit risk boggles the mind of anyone who prefers market solutions. Fannie Mae guarantees or owns more than $2.7 trillion in mortgages. Freddie Mac guarantees or owns more than $1.7 trillion. Fannie and Freddie are said to be “implicitly guaranteed” by the U.S. Treasury, but whatever it is called, the guarantee is real. This was proved beyond doubt by the $187 billion government bailout they got when they went broke in 2008.

Then we have Ginnie Mae, a wholly-owned government corporation which is explicitly guaranteed by the U.S. Treasury. It guarantees another $1.7 trillion in mortgage-backed securities, with its total slightly greater than Freddie’s.

The three together absorb $6.2 trillion of mort- gage credit risk, all of it ultimately putting the risk on the taxpayers. This is more than 59 percent of the total mortgage loans outstanding. The U.S. government is in the mortgage business in a big way!

But this is not all. There is, interlocked with Ginnie Mae, the Federal Housing Administration [FHA], a part of the federal Department of Housing and Urban Development. The FHA is the U.S. government’s official subprime lender. (Of course, they don’t say it that way, but it is.) It insures very low down-payment and otherwise risky mortgage loans to the total amount of $1.4 trillion.

The federal Veterans Administration insures mortgages for veterans of the armed services to the amount of $596 billion.

The Federal Home Loan Banks, another government-sponsored housing finance enterprise, have total assets of $1.1 trillion.

Even the federal Department of Agriculture gets into the mortgage credit act. It guarantees housing loans of $108 billion.

A more recent, but now huge government player in mortgage credit is America’s central bank, the Federal Reserve. The Fed is the largest investor in mortgage-backed securities in the world, owning $1.8 trillion of very long term, fixed rate MBS guaranteed by Fannie, Freddie and Ginnie. So, one part of the government guarantees them, taking the credit risk, and another part of the government buys and holds them, taking the interest rate risk.

How does the Fed finance this long-term investment? By monetization – creating floating-rate deposits on its own books. This results in the Fed having the balance sheet structure of a 1980s American savings and loan: holding very long-term fixed-rate assets financed with variable rate liabilities. There is no doubt that this would have astonished and outraged the founders of the Federal Reserve System, and that for most of the Fed’s history, its new role as mortgage investor would have been thought impossible.

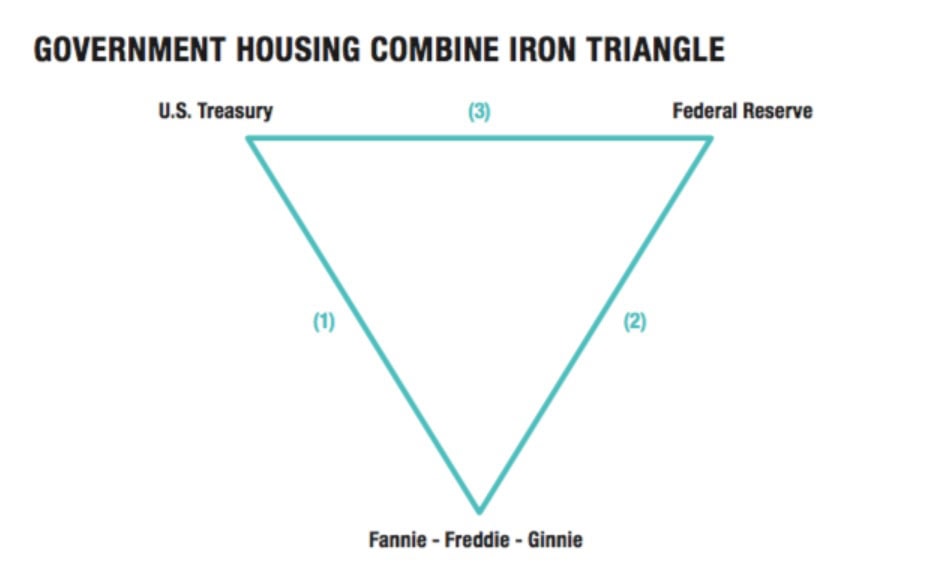

We can see that the U.S. now has a giant Government Housing Combine. It has a lot of elements, but most importantly there is a tight interlinking of three principal parts: the U.S. Treasury; the Federal Reserve; and Fannie-Freddie-Ginnie. It is depicted in Figure 1 as an iron triangle.

Let us consider each leg of the triangle:

(1) The U.S. Treasury guarantees all the obligations of Fannie, Freddie and Ginnie, which allows them to dominate the mortgage- backed securities market. The Treasury owns 100 percent of Ginnie, and $189 billion of the senior preferred stock of Fannie and Freddie, plus warrants to acquire 79.9 percent of Fannie and Freddie’s common stock for a minimal price, virtually zero. Essentially 100 percent of the net profits of Fannie and Freddie are paid to the Treasury as a dividend on the senior preferred stock. Fannie, Freddie and Ginnie are financial arms of the U.S Treasury.

(2) The Federal Reserve owns $1.8 trillion in mortgage-backed securities, mostly those of Fannie and Freddie. Without monetization of their securities by the Fed, Fannie and Freddie would either have much less debt, or have to pay a significantly higher interest rate to sell it, or both. Without the guarantee of the Treasury, Fannie and Freddie could sell no debt whatsoever. The Fed earned $46 billion on its MBS investments in 2016, almost all of which was sent to the Treasury. The U.S. government is reducing its budget deficit by running its big mortgage business.

(3) The Federal Reserve finances the Treasury, as well as Fannie and Freddie. The Fed owns $2.5 trillion of long-term Treasury notes and bonds, in addition to its $1.8 trillion of MBS. Almost all, about 99 percent, of the Fed’s profits are sent to the U.S. Treasury to reduce the budget deficit.

You can rightly view all this as one big government mortgage business. As my Danish colleague wondered, who is the socialist?

We asked before what this massive government intervention in housing finance has achieved. There are two very large, but not positive, results: inflating house prices and inducing higher debt and leverage in the system. Government guarantees and subsidies will get capitalized into house prices, and with the impetus of the Government Housing Combine, U.S. average house prices are now back up over their bubble peak. This makes it harder for new households to buy a house, and it means on average they have to take on more debt to do so.

Confronted with these inevitable effects, one school of politics always demands still more government guarantees, more debt, and more leverage. This will result in yet higher house prices and less affordability until the boom cycle ingloriously ends. A better answer is instead to reduce the government interventions and distortions, and move toward a housing finance sector with a much bigger private market presence.

I propose the goal should be to develop a U.S. housing finance sector in which the mortgage credit risk is at least 80 percent private, and not more than 20 percent run by the government. That’s a long way from where we are, but defines the needed strategic direction.