Courts need a better appreciation of the principles of depreciation

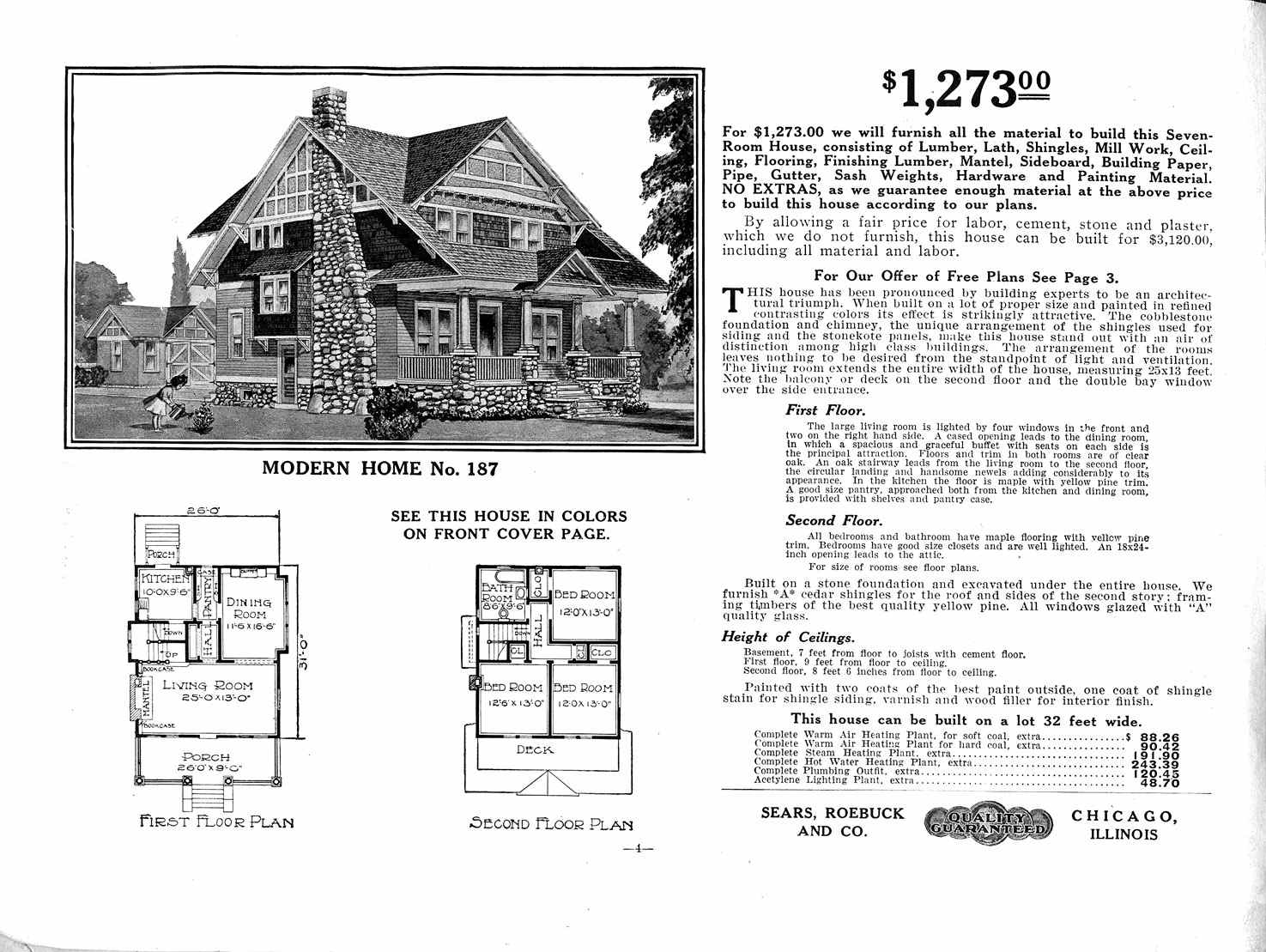

Post-World War II, the United States experienced a simultaneous boom of babies and buildings. To keep pace with the need for new development, homes literally could be ordered out of a Sears catalogue.

{kind=link}

The true expense of such homes was not found in the cost of the building supplies, but rather in the labor necessary to construct the structure. A Sears home available for $1,000 would, with the cost of construction figured in, run closer to $3,000.

That distinction, between the cost of materials and the cost of labor, is at the core of a current controversy about how replacement costs should be calculated.

Replacement-cost calculations are utterly uninteresting to most people, right up until they experience a loss. At that point, those uninterested people are surprised to learn that, if their homeowners insurance policy spells out that they are entitled only to the “actual cash value” of certain features of their home (a roof, a deck, etc.), then damage claims will subtract from the replacement costs any depreciation stemming from the wear and tear the home would have experienced over time.

In 2002, the Oklahoma Supreme Court was prompted by a U.S. District Court to answer this question: “In determining actual cash value, using the replacement costs less depreciation method, may labor costs be depreciated?” That is, when determining the amount to be paid out to satisfy a claim, is it appropriate to distinguish between the materials, which obviously depreciate over time, and the labor use in construction?

The Oklahoma court ruled against such distinctions because “labor is a part of the whole product, it is included in the depreciation of the roof.” At bottom, insurance is designed to return claimants to their pre-loss condition. If a tree lands on a homeowner’s seriously dilapidated porch, the value of that porch (which might effectively be nothing) is all the homeowner is entitled to.

But in the case of, for instance, the owner of the Sears home, the materials and labor were purchased separately. This can be cause for confusion. Recently, courts and even some departments of insurance have embraced that confusion and departed from the Oklahoma court’s reasoning. The counter argument – elucidated earlier this year by a U.S. District Court in Kentucky – holds that while construction materials age, labor does not:

Labor is not subject to wear and tear. Indeed, the cost of labor to install a new garage would be the same as installing a garage with 10 year old materials. In other words, depreciated labor costs would result in under indemnification. As the insurance contract is one for indemnity, depreciating the cost of labor violates the contract.

Of course, it’s true that labor is not subject to wear and tear. But that obfuscates the larger point, which is that any produced item is composed of a mixture of labor and material. It is that item which depreciates, not its component parts, which ultimately are indistinguishable.

The Oklahoma Supreme Court’s reasoning rests soundly on a theory of property not unlike that of 17th century British philosopher John Locke. A home’s roof is not just the materials needed to create it or the labor for its construction. The roof only exists when the materials and labor are mixed.

Were an insurance policy drafted to cover labor and materials separately, it would be reasonable for a claimant to assume that labor would not depreciate. But in virtually all cases, claimants insure their structure as a whole. Put another way, the relative component parts of labor and materials aren’t relevant to the depreciation of an item itself.

A practical consequences of the Kentucky court’s decision to not allow for depreciation of labor in “actual cash value” policies will be that like items are treated differently. For instance, it is possible that one contractor who got a good deal on materials, but overcharged for labor, would construct a deck that is deemed more valuable than another contractor who paid market price for materials and a regular price for labor, even if they were the same deck and depreciated at the same rate. Again, the value of the item itself is determinative of the value of a claim because the policy, in all likelihood, covers the item itself.

That courts are choosing to ignore the distinction between the antecedent conditions of an item and the item itself is troubling. That the colloquial wisdom upon which such decisions are being made is creeping into quasi-legislative determinations of state insurance departments is more problematic. Depreciation of labor is an affordability mechanism by any other name. Prohibiting it will hurt the very insureds that insurance departments are attempting to assist.